November 14, 2024

Co-Payment: What it Means and Why it Matters

Co-payment, or “co-pay,” is a common term in medical insurance and takaful plans. This guide explains what co-payment means, how it works, and why knowing it can help you better manage your healthcare expenses.

In today’s complex healthcare landscape, terms like “co-payment” or “co-pay” often come up when discussing medical insurance and takaful plans. While it sounds technical, co-payment is actually a simple concept that can significantly impact how you manage your healthcare costs. Here, we break down what co-payment is, how it works, and why understanding it is crucial for managing your current and future medical expenses.

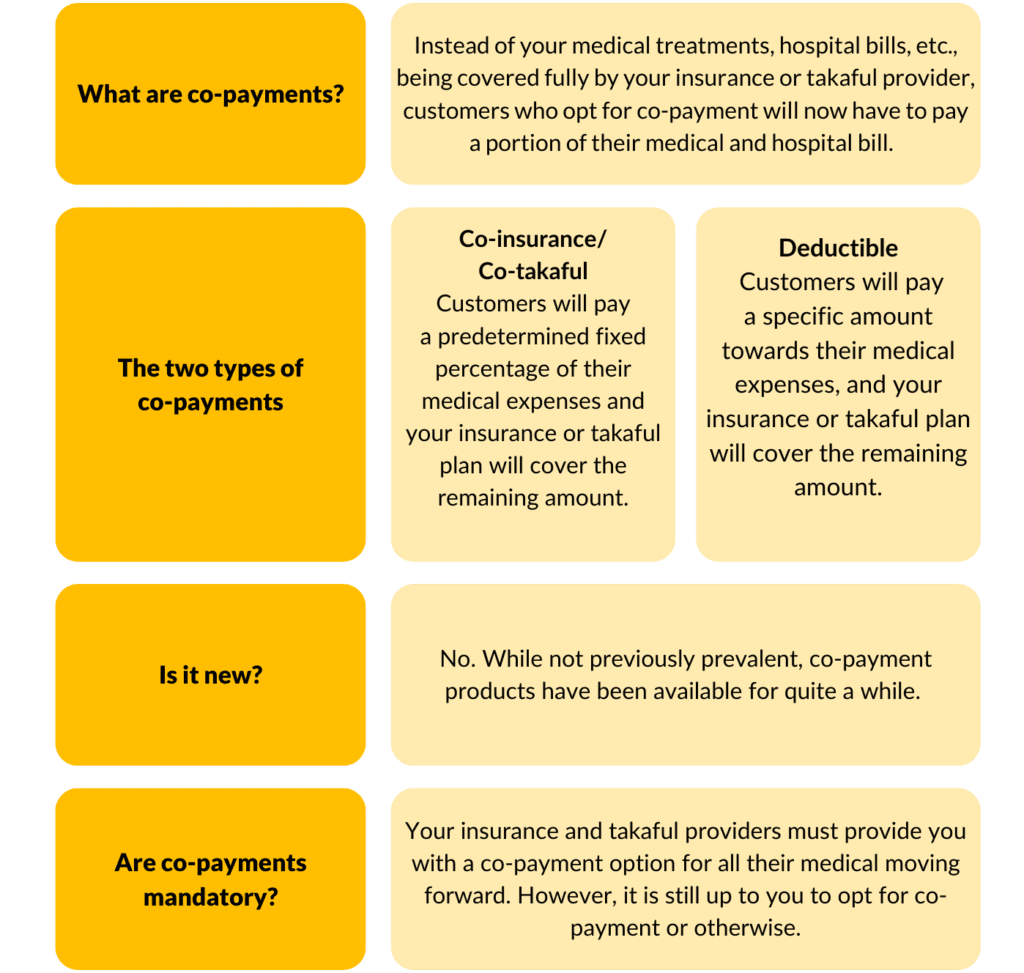

Co-Payments: What It Is

Co-payments are a new requirement by Bank Negara Malaysia aimed at combatting the rising costs of medical inflation within the country. At 12.6% in 2023, Malaysia’s medical inflation cost was more than double the global average of 5.6%, forcing insurance and takaful providers to increase their premiums/contributions to ensure they can continue providing Malaysians with the funds to cover their healthcare and medical costs. This left policy owners and certificate participants with two options:

- Increase their monthly payments to maintain their existing coverage and benefits, or

- Downgrade to a lower plan with lower coverage

In order to support the insurance and takaful industry and ensure it remains sustainable and affordable, co-payment has been made a mandatory option for all new medical plans starting 1 September 2024.

But what does that mean, exactly?

How It Works

These findings are quite troubling as most Malaysians are clearly not financially prepared if something unwanted were to happen.

Bank Negara Malaysia has set a minimum co-payment amount of:

- Co-insurance / co-takaful: 5% of the total hospitalisation discharge bills per year.

- Deductible: RM500 per policy/certificate year, regardless of the hospitalisation discharge bill amount.

No maximum limit has been set, meaning insurance and takaful providers can set a higher co-payment amount if they deem it necessary.

To ease customers into this new concept and simplify the payment process, Etiqa has decided to offer the deductible co-payment option for all our new medical plans starting with the minimum amount of RM500 per policy/certificate year.

While RM500 is the minimum deductible amount, customers can choose a higher co-payment amount – if there’s an option from your provider in exchange for lower monthly insurance premiums and takaful contributions.

All existing medical plans that are without co-payment can continue with no changes and customers can buy existing insurance and takaful plans that do not have co-payment should the insurer or takaful operator still offer it.

How Co-Payment Benefits You

Co-payment was introduced to counter the sharp increase in insurance premiums and takaful contributions. By selecting a co-payment plan, customers can enjoy a lower premium for medical protection. In addition, it is hoped that the introduction of co-payment will encourage customers to be pay more attention to the medical treatments being offered to them and curb medical inflation in the long run.

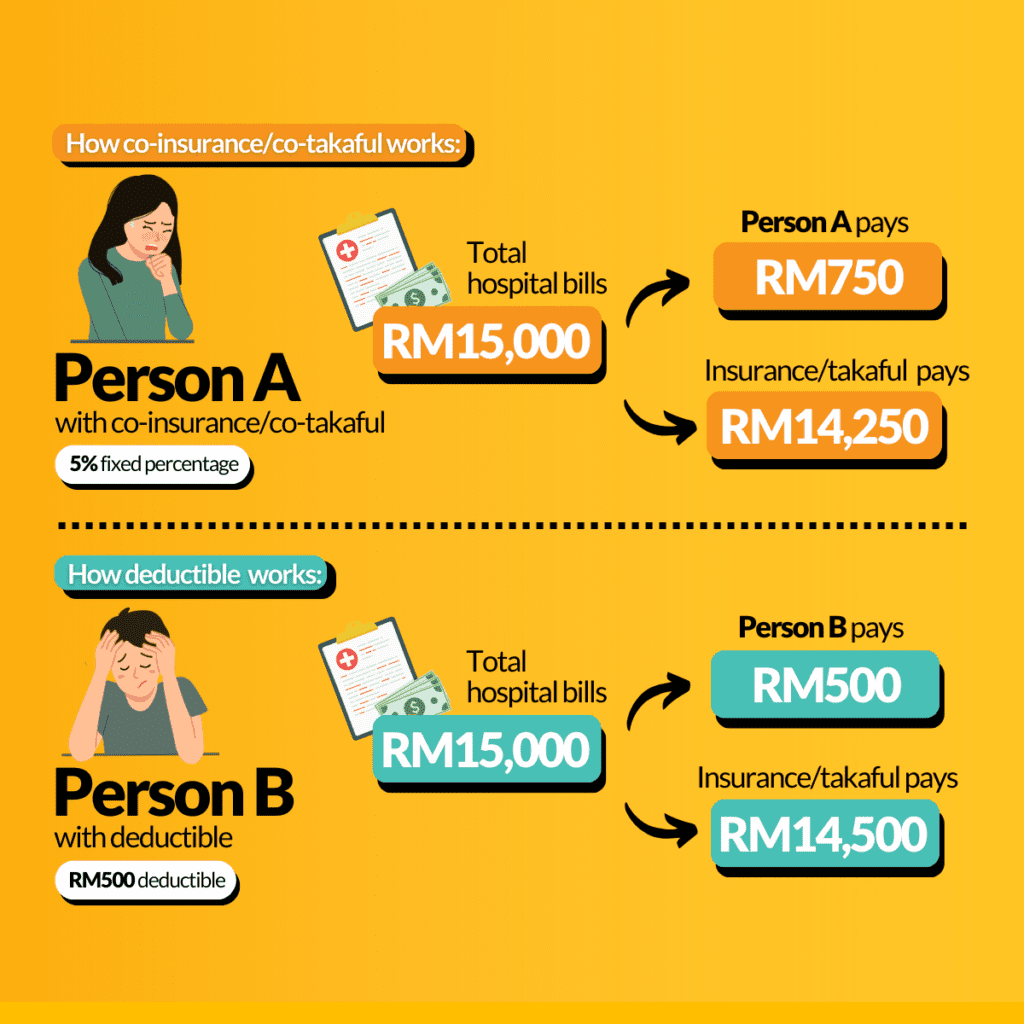

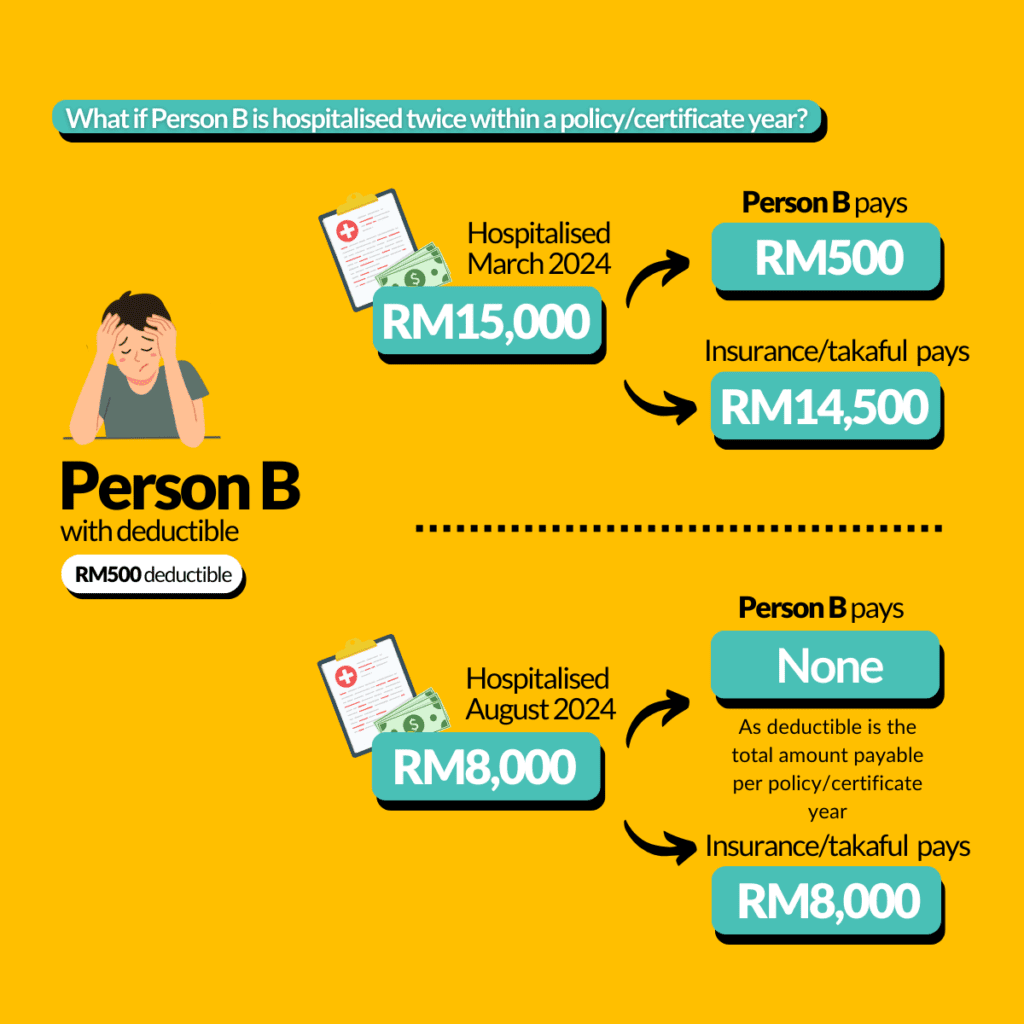

Here are some scenarios on how co-payment works:

Notes:

i. Co-payment scenarios are based on BNM’s minimum requirement of 1 time payment per policy/certificate per year upon hospitalisation

ii. Person covered commenced their coverage in the year 2024

If you’re young, healthy, and fit with no family history of serious medical illnesses, co-payment is a great option to consider if you would like to get quality protection at more affordable prices.

How Co-Payment Affects Your Existing Etiqa Protection

Etiqa’s co-payment type for all co-payment plans is deductible.

Changing your current protection to a deductible plan is not mandatory. However, due to Malaysia’s high rates of medical inflation, existing plans without deductible will no longer be enhanced with new features. Furthermore, protection plans with deductible may continue experiencing an increase in premiums/contributions.

To help you make an informed decision when reviewing your medical protection, and to understand how deductible fits into your overall healthcare coverage, here are some factors to keep in mind:

- Amount of co-payment: While the minimum deductible amount is RM500 per year, the amount can vary between policies/certificates and services. Be sure to review your plan’s details so you know exactly what to expect.

- Annual limits: All insurance policies and takaful certificates have an annual limit threshold. An increase in premiums and contributions may cause this amount to deplete faster if you decide not to go with co-payment.

- Coverage of services: Deductible will apply to all medical services except the following:

- Emergency procedures including accidents.

- Outpatient treatments for follow-ups on critical illnesses, including cancer treatments and kidney dialysis.

- Treatments sought at a government healthcare facility.

Instead, if applicable, your coverage will kick in as usual without you having to pay the deductible amount.

If you would like to know more about co-payment and how it affects your current medical protection plan, talk to your agent or contact us at Etiqa.

Etiqa has a variety of takaful and insurance products to support your needs. Visit us on www.etiqa.com.my to discover more. Check out our life stages quick guide to help you understand your protection needs better.